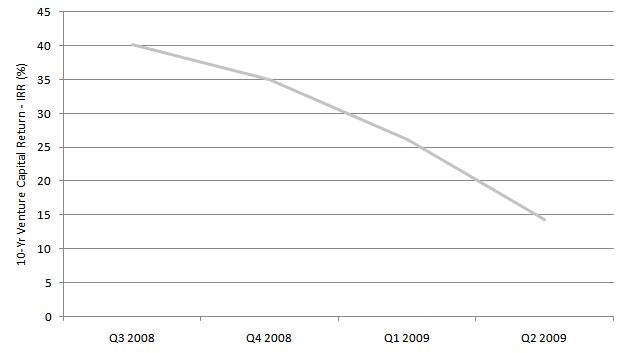

Over the past year there’s been a lot of talk about how venture capital returns over a ten-year time horizon will no longer look so hot once this year is out. This is because after this year the ten-year timeframe will no longer include returns from 1999 – a year featuring huge exits through quick IPOs in what was the last year before the bursting of the tech bubble. The 10-year venture capital return currently stands at 14.3% (as of 6/30/09 – VC returns are always on a quarter or quarter and a half lag), but has been in a steady decline. There’s been some speculation that the decline in this return will have a negative impact on the venture industry’s attractiveness to investors, but I don't think that is necessarily the case.

Over the last four quarters, the 10-year return has tumbled from over 40% to 14%. For a visual, here’s what the recent drop in the 10-year return looks like:

Before going further, here’s some background on how the return is calculated:

The 10-year return is an end-to-end venture capital fund-level return, meaning it looks at the fund-level (read: not company level) cash flows – to LPs only, meaning it is net of fees and carried interest ( a good thing because this is the true level of return an investor in venture capital funds would have received). The return is a standard IRR calculation except that it in the period in which it starts, in this case the second quarter of 1999, the cash flow pulls in the negative starting net asset value of all the funds comprising the index. Going forward, all contributions and distributions are netted to get the cash flows for each quarter (for timing purposes, the figure is assumed at the midpoint of each quarter). For the final quarter of the calculation the current net asset value of all the funds in the index is added in as a positive cash flow.

What’s the recipe for this drop in the 10-year return? For one, huge IPOs started tapering off after 1999 while at the same time, inflated valuations made the beginning negative cash flow much larger and tougher to overcome, dragging down returns. Then add in the fact that there hasn’t been another period of fantastic exits since, and that the past year has been absolutely dismal for venture-backed exits and you get a free-falling 10-year venture capital return.

But how important is the 10-year return really? The whole notion that the 10-year return’s fall will have a negative impact on the venture industry is actually hugely flawed. The pure numerical drop in the 10-year return should not be what deters investors. Why? Because sophisticated investors (limited partners) are smart enough to not have been looking at the 10-year return anyway. If anyone looked at the 10-year return as their reason to invest in venture, they clearly do not understand the asset class enough to be making decisions on investing in it. 10-years, despite being a round number, is just as arbitrary as any other number. Nothing makes it different than looking at 9 or 11 years. Even if you are comparing to public markets. The only thing that makes this current case unique is that we are on the brink of excluding a great period for venture. But by now, most investors have come to accept the tech bubble as an aberration, and new expectations for venture returns are much more tempered, albeit still relatively high because of the illiquidity and risk.

Plus., if you want to get technical, the 10-year return isn’t realistic for investors because to have gotten those 10-year returns they would have had to have gotten into funds in the prior one to four vintage years – the ones which were actively investing prior to the bubble and able to exit during the bubble.

Finally, no legit VC I can think of is selling their fund based on 10-year industry returns. In fact they probably look to avoid having to talk about the bubble years because the business is so different now. What happened 10 years ago is pretty much irrelevant. VCs are judged on their performance over the last five years, how their strategies can take advantage of the current environment, and their ability to exit deals over the past year and going forward.

What the drop in 10-year return does more than anything is highlight a major shift in the venture industry - a shift that investors and VCs were aware of years ago and probably ever since the bubble burst. This drop in the 10-year return is not new information and could have esily been predicited a few years ago. We’ve gone from some 250 venture-backed IPOs in 1999 to just 10 so far this year. We know there will be attrition in the industry, but investors that stick with venture capital should be better off because of it. Innovation continues unabated and top mangers continue to provide quality returns through building and growing companies - the way it should be.