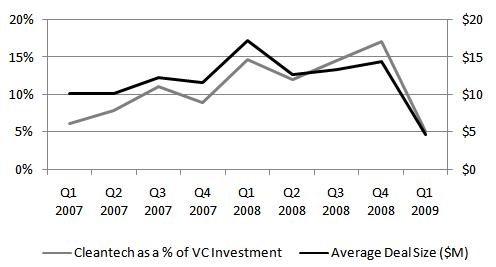

Not only has cleantech investment by venture capitalists dropped off a cliff recently, but the average deal size has fallen significantly too – from $14.5 million in Q4 of 2008 to just $4.7 million at the end of the first quarter of 2009 (PwC/NVCA MoneyTree). Clearly VCs have figured out that deals that eventually need to scale to utility size are trouble. Still, I’ve heard many people point to the lack of project financing or debt (credit crunch) as to why things have stalled. In fact, venture-backed algae company GreenFuel Technoloogies shut down this week. The reason? They claim they were a victim of the credit crunch. But should VCs really have been reliant on project finance in cleantech investments in the first place?

Take a look at the chart below. I’ve graphed the average venture cleantech deal size over time, which I mentioned has fallen by almost $10 million, mainly because there were no major $100 million+ rounds. But what really shows how disproportionally cleantech was reliant on large scale financing is how much investment fell as a percentage of all venture investment.

It helps to put the data in this context because it shows that other sectors, while still experiencing declines in dollar amounts, were not affected nearly as much by the lack of large deals. And by other sectors, I’m talking mainly about technology deals, which have always been mainstays of venture investment. By and large, they are less capital intensive and, really, it’s where venture’s expertise lies. This level is where I think cleantech venture investment belongs.

The current average deals sizes (around $5 million) in cleantech are much more reasonable and the capital going in is still adequate enough support innovation. A recent New York Times article covers the shift in this direction. Liquidity-wise, hybrid tech/cleantech deals have much more promise too. Of potential acquisition targets, they seem like they are the most attractive since they can still produce great return multiples in reasonable amounts of time. Scaling is faster and cheaper - all VCs know this. So instead of trying to hit “grand slams” with large, utility scale projects it may be better to leave those to the utilities and GE’s of the world. VC’s should not be chasing stimulus money, or be in denial about the capital intensity of most renewable energy investments. To me, there’s nothing wrong or concerning about the decline in cleantech venture investment if it represents a shift back to venture’s roots.

A point on the data I used: I realize there are a number of sources I could have used (MoneyTree, The Cleantech Group, VentureSource, Greentech Media, etc.). And they all report different figures due to differing methodologies. The key is not to get caught up in the differences there – they all show the same trend which is the most important thing, particularly when looking at industry data on private equity, which always inconsistent among the different sources.