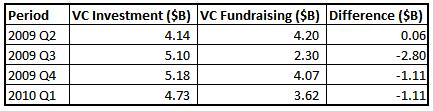

I was about to do an update on the Venture Capital Overhang I’ve been tracking, but instead of the typical chart this time around I thought it’d share something interesting that stood out - for the last three quarters we’ve now seen US venture capital investment outpace fundraising (and the quarter before it was almost even):

The only other time in recent history where we’ve seen investment activity even come close to surpassing fundraising was in 2003 following the bursting of the tech bubble. What does this mean? We have numbers clearly indicating that a fundamental shift in the industry is underway. In previous posts, I’ve mentioned how fundraising could not forever outpace investment as dramatically as it had been doing so over the past decade (creating an ever increasing “overhang” of un-invested capital, or dry powder). Fundraising has now slowed dramatically, while venture capitalists rightfully continue to invest in what is a good environment to be doing so in.

A drop in fundraising was expected, but we may now have a “new normal” for fundraising levels. There is clearly a new standard for raising capital now, especially with so many limited partners still skeptical of the asset class. At first a fundraising slowdown was blamed on the “denominator effect,” and later it was said that many limited partners were waiting to get a clearer picture of their allocation balance before beginning to commit again. But the truth is that most limited partners will not return to commitment levels of the past and therefore we will see a natural attrition of firms in the future.

Investment may outpace fundraising for a while - until fringe firms run out of capital and are unable to raise new funds. Just as I had said fundraising could not outpace investment forever, the converse holds true as well and we surely will not see investment outpace fundraising forever either. Think of this period (of investment outpacing fundraising) as sort of a market correction. When we had huge overhangs of capital, venture capitalists knew there were others out there with capital to deploy as well which drove up valuations and reduced returns. What we should see after this correction is fewer firms - this means higher quality firms will remain, investing in better deals at better valuations and generating better returns.

The differential in fundraising and investing should be interesting to monitor. Too large of a crossover into fundraising outpacing investment again may signal another bubble, while a leveling out should indicate a healthier venture capital industry.

Note: Data from PwC, Thompson Reuters and the NVCA. And for clarity, the VC overhang now stands at $88 billion – down from $89 billion at the end of 2009.