The Real Impact Of Overlooked Fund Return Considerations

The Private Equiteer recently brought up an aspect to private equity and venture capital returns that is often overlooked and unaccounted for: The fact that investors (limited partners) in funds have to set aside or plan around the capital they have committed to a fund. For those less familiar with private equity, investors in funds do not pay in the full amount they decide to invest in a fund right away. Instead, capital is called by the general partner as the fund makes new investments. Rarely do limited partners set aside their full commitment to a fund and hold cash to meet capital calls as they come. Most model around expectations provided by fund managers and hold only the amount of cash necessary to meet capital calls.

The Private Equiteer argues that opportunity cost of holding cash, or the risk of default associated with reserving inadequately should be factored into private equity returns. I would agree that there is some opportunity cost involved, but the simple fact is that virtually no limited partner holds the full amount of a commitment to a fund it has decided to invest in as cash – only for short periods to meet imminent capital calls, which in the grand scheme probably has a negligible effect on returns. There’s also a very limited chance that a limited partner defaults on a capital call. It’s extremely rare, and even if it does happen, there are remedies that would allow the limited partner to continue investing in the fund – rarely would all value be lost.

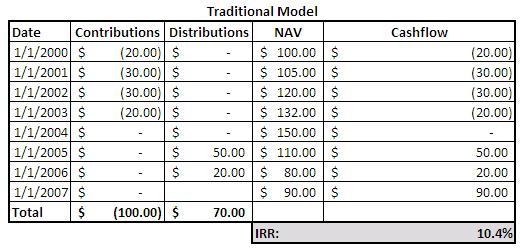

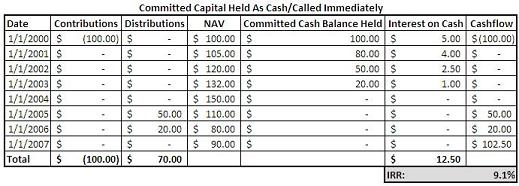

The reason these two issues aren’t talked about too much is probably because they’re not really major issues to begin with. Putting aside the risk of default (which is incredibly small), let’s take a look at the effect holding committed capital as cash would have on a fund’s return. If you remember, in my model for a crowdsourced venture capital fund, I suggested that all committed capital would have to be called at the onset of the fund to make things logistically simpler – perhaps as the private equity and venture capital industries evolve, we’ll see more of this. Below I’ve modeled out a hypothetical private equity or venture capital fund’s cash flows under a normal model (which assumes that cash comes in right at the time of a capital call) and also for a model where cash is held/called at the onset of a fund (same impact on returns). I’m using 5% as an interest rate for the cash and the rest of the cash flows for both models are the same. Here’s what we get:

As you can see, there is clearly an impact on the fund’s IRR - a difference of around 1.3% in this case, but with a return multiple of 1.6x under both scenarios. Is this a significant difference? I would say it’s definitely material, but it depends on the investor. The difference is probably significant enough to impact investment decisions and overall portfolio performance, and its why funds do not call capital upfront (negative impact on IRR, even though all other performance is the same) and why limited partners don’t hold cash. They assume they can earn even more than the 5% I modeled in on their cash. The only benefit derived from calling capital upfront or holding a commitment as cash is eliminating the risk of default, but as I mentioned before, it’s such a small risk in the first place that it does not make sense to protect against in such a way. That said, I do stand by the idea that for different models such as a crowdsourced fund, you would still want to call all capital upfront, even if you sacrifice a bit of your IRR.

AV

AV

Reader Comments