VC’s: How To Benchmark Yourselves Properly

Plenty of VCs are guilty of deceitfully presenting fund performance – especially when it comes to benchmarking themselves against their peers in marketing materials. There’s a reason why so many LPs complain about almost every VC claiming to be “top quartile.” When raising new funds or providing updates, you too frequently find venture capitalists benchmark their performance improperly, often in an attempt to make themselves look better. Instead of these attempts, existing and prospective LPs would probably find it much more amicable if VCs candidly presented their relative performance - in fact, being candid in presenting performance and benchmarking goes a lot further than you would think with most LPs. Here’s a guide on how to go about benchmarking properly and in a way that LPs will surely appreciate:

Selecting a Benchmark:

Use the Cambridge Associates Benchmark Statistics - don’t even consider any alternatives. Their benchmarks are far and away the most comprehensive. A common alternative you see is the ThomsonReuters (Venture Economics) benchmarks but they fall so short of Cambridge in terms of sample size that their statistical validity is questionable - sophisticated LPs are aware of this issue. The Cambridge benchmarks exhibit slightly higher returns because of their selection bias (all funds that Cambridge clients are in get pulled in so some consider it more of an “institutional quality benchmark”), but they are the industry standard and using anything else immediately raises doubts for LPs.

Don’t have access to their quarterly benchmark statistics? Simply contact them and participate in their quarterly survey and you’re receive the benchmark statistics free of charge. You’ll have to provide your quarterly financials to them but don’t worry, all data is kept confidential and your performance remains anonymous. They’ll even sign an NDA if you ask them to.

What to Present:

Determining the Proper Vintage Year: Cambridge Associates determines a fund’s vintage year based on the partnership’s date of legal formation - not by when a fund holds its final close and not by when a fund started investing. This means that under most circumstances you should do the same, unless there’s a special case where a fund took over a year to raise or if the fund was legally formed so late in a year and didn’t start investing until late in the next year that its most logical to use the next vintage year. If either case applies, make sure you footnote the situation properly.

Determining the Proper Asset Class: Usually it’s not difficult deciding whether the venture capital or private equity benchmark is most appropriate. But in some cases where a fund has a later stage or growth equity strategy, LPs like to see it benchmarked using private equity benchmarks. If you have a strategy that straddles venture and private equity, consider using both benchmarks.

Performance: You must of course show IRR, but make sure it is the IRR NET TO LPs (net of fees and carry) not the gross fund IRR. Nothing is worse than a VC that either purposely or inadvertently shows just gross IRR and then even worse, benchmarks it against the net to LP benchmark. It’s ok to show a fund’s gross IRR but if you decide to do so, you must also show the net IRR as the next line item. Generally, when benchmarking you want to show just the Net IRR because if there’s a large discrepancy between the net and gross, it draws attention to the effect management fees and carry is having on the return to LPs.

In addition to the IRR also show and benchmark the distributed/paid-in and total value/paid-in multiples. Showing fund level cash flows is a plus too. The reason for showing the multiple is to help iron out some of the effects timing has on the IRR and give a truer sense of the fund’s performance. This goes back to being candid – you don’t want to omit multiples if IRR has been boosted by a quick exit, and conversely, for older funds you might actually be doing yourself a disservice by not including the multiples if IRR has been dragged down because of timing.

Not Meaningful Performance: A general rule you can follow is that a fund’s performance is not meaningful and thus okay not reporting on and benchmarking if there has been less than three years of activity. Just make sure you footnote why you have decided that a fund’s performance is not meaningful and why it hasn’t been benchmarked. But also be sure to have the performance handy and expect to provide it if an LP asks for it.

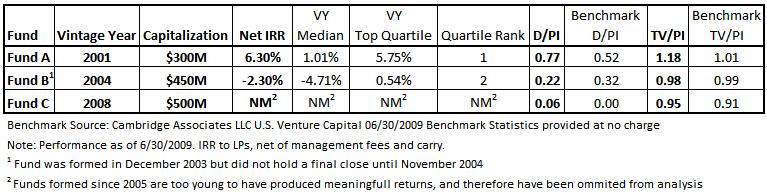

Here’s an example of how fund benchmarking should look (note: figures are fictional):

Note that these guidelines apply to sharing fund level performance only and that the guidelines for sharing company level returns are much different – something I’ll eventually post about later. In the meantime, feel free to provide feedback or ask questions about these guidelines.

AV

AV